Cosa sono duration e convexity?

Quando si investe in obbligazioni con cedola, si usa una metrica chiamata "duration" per misurare quanto il prezzo dell'obbligazione sia sensibile alle variazioni dei tassi di interesse. Le banche usano uno strumento di gap management per assicurarsi che le duration delle loro attività e passività siano uguali. Questo aiuta a proteggere la loro posizione complessiva dall'impatto delle variazioni dei tassi di interesse.

Fondamenti

La gestione del rischio negli investimenti a reddito fisso implica l'utilizzo di duration e convexity. La duration valuta la reattività del prezzo di un'obbligazione alle fluttuazioni dei tassi, mentre la convexity riguarda l'interazione tra prezzo e rendimento dell'obbligazione in presenza di variazioni dei tassi di interesse.

Per le obbligazioni con cedola, gli investitori ricorrono alla duration come metrica cruciale per valutare la sensibilità del prezzo alle variazioni dei tassi. Poiché le obbligazioni con cedola prevedono più pagamenti durante la loro vita, diventa essenziale per gli investitori a reddito fisso quantificare la scadenza media dei flussi di cassa attesi dell'obbligazione. La duration funge da misura concisa della scadenza effettiva dell'obbligazione, offrendo agli investitori uno strumento efficiente per valutare l'incertezza nel controllo dei portafogli.

Duration di un'obbligazione

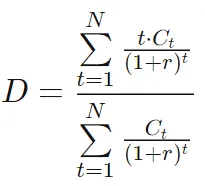

Nel 1938 l'economista canadese Frederick Robertson Macaulay introdusse il termine "duration" per rappresentare la scadenza effettiva di un'obbligazione. Il suo calcolo propone di determinare la media ponderata dei tempi di pagamento di ogni cedola o capitale emesso dall'obbligazione. La formula della duration di Macaulay è espressa come segue:

dove:

- D = Duration di Macaulay dell'obbligazione

- T = Numero di periodi fino alla scadenza

- i = Il periodo i-esimo

- C = Il pagamento della cedola periodica

- r = Il rendimento periodico a scadenza

- F = Il valore nominale a scadenza

Gestione di portafogli a reddito fisso: svelare l'importanza della duration

Il ruolo della duration nella gestione efficace dei portafogli a reddito fisso è sfaccettato:

- La duration serve come misura statistica concisa, racchiudendo la scadenza media effettiva di un portafoglio.

- Gioca un ruolo fondamentale nell'immunizzare i portafogli contro le incertezze delle oscillazioni dei tassi di interesse.

- Fornisce una stima affidabile della sensibilità ai tassi insita in un portafoglio.

Caratteristiche rilevanti della duration

- Per le obbligazioni zero-coupon, la duration coincide con il tempo alla scadenza.

- A parità di scadenza, tassi di cedola più elevati contribuiscono a una durata inferiore a causa dei pagamenti anticipati delle cedole.

- Tenendo costante il tasso di cedola, la duration di solito aumenta con il tempo alla scadenza, salvo eccezioni come le obbligazioni ad alto sconto, dove la duration può diminuire con scadenze più lunghe.

- La duration delle obbligazioni con cedola aumenta quando i rendimenti a scadenza sono più bassi, mentre per le zero-coupon la duration equivale al tempo alla scadenza indipendentemente dal rendimento.

- La duration di una rendita perpetua a tasso costante si calcola come (1 + y) / y, illustrando una significativa differenza fra scadenza e duration. Ad esempio, a un rendimento del 10% la duration di una perpetuità che paga $100 all'anno è di 11 anni, mentre a un rendimento dell'8% si estende a 13,5 anni. Questo sottolinea la divergenza tra la scadenza (infinita) e la duration (11 anni con rendimento al 10%). La predominanza dei flussi di cassa ponderati al valore attuale nelle fasi iniziali della perpetuità influenza il calcolo della duration.

Gestire i gap di duration nelle banche

Nel settore bancario, spesso si verificano disallineamenti nelle scadenze di attività e passività. Le passività bancarie, principalmente depositi dei clienti, tipicamente presentano caratteristiche a breve termine con bassa duration. Al contrario, le attività di una banca, composte principalmente da prestiti commerciali e al consumo o mutui, tendono ad avere durate più lunghe, rendendole più sensibili alle variazioni dei tassi. Aumenti inattesi dei tassi possono portare a cali significativi del patrimonio netto di una banca se il valore delle attività diminuisce più delle passività.

Il gap management emerge come strategia di mitigazione del rischio diffusa, mirata a minimizzare il "gap" tra le duration di attività e passività. I mutui a tasso variabile (ARM) svolgono un ruolo centrale in questa strategia, contribuendo a ridurre la duration dei portafogli di attività bancarie. A differenza dei mutui tradizionali, gli ARM mantengono il loro valore durante aumenti dei tassi di mercato, poiché i loro tassi sono legati al tasso corrente.

Al contrario, sul lato delle passività, l'introduzione di certificati di deposito (CD) a termine più lunghi serve ad estendere la duration delle passività bancarie, contribuendo a mitigare il gap di duration.

Esplorare il gap management

Il gap management è uno strumento strategico che le banche impiegano per allineare le duration di attività e passività, garantendo una solida difesa dagli impatti delle variazioni dei tassi di interesse. Il presupposto fondamentale prevede il mantenimento di attività e passività di dimensioni approssimativamente equivalenti, permettendo alle variazioni dei tassi di esercitare un'influenza uguale su entrambe e minimizzando qualsiasi effetto sul patrimonio netto. Raggiungere l'immunizzazione del patrimonio netto richiede una duration di portafoglio o un gap pari a zero.

Diversamente dalle banche, istituzioni con obblighi futuri a tasso fisso, come fondi pensione e compagnie assicurative, operano con attenzione ai futuri impegni. Ad esempio, i fondi pensione devono assicurare fondi adeguati per mantenere i flussi di reddito dei pensionati. Con l'oscillare dei tassi, il valore delle attività del fondo e il reddito che esse generano variano di conseguenza. In risposta, i gestori di portafoglio possono cercare di immunizzare il valore accumulato futuro del fondo contro potenziali movimenti dei tassi, assicurando che attività e passività con duration corrispondenti proteggano la capacità dell'istituzione di adempiere agli obblighi, indipendentemente dalle variazioni dei tassi.

Comprendere la convexity nella gestione a reddito fisso

Nella gestione a reddito fisso, la duration ha limiti come indicatore di sensibilità ai tassi. Nonostante la sua capacità di calcolare una relazione lineare tra prezzo e variazione del rendimento, la relazione pratica mostra una convessità.

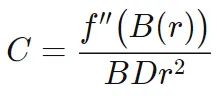

La convexity, che misura la curvatura delle variazioni di prezzo di un'obbligazione rispetto alle fluttuazioni dei tassi di interesse, corregge questo limite valutando la variazione della duration al mutare dei tassi. La formula è rappresentata come:

dove:

- f′′ = Derivata di secondo ordine

- B = Prezzo dell'obbligazione

- r = Tasso di interesse

- D = Duration

Tipicamente, le obbligazioni con cedole più alte mostrano convexity minore, poiché un'obbligazione al 5% è più sensibile alle variazioni dei tassi rispetto a una al 10%. Le obbligazioni callable, che incorporano un'opzione di rimborso anticipato, presentano convexity negativa quando i rendimenti scendono troppo, risultando in una diminuzione della duration con rendimenti decrescenti. Le zero-coupon vantano la convexity più alta, con relazioni valide solo a parità di duration e rendimento a scadenza. Notoriamente, le obbligazioni ad alta convexity mostrano maggiore sensibilità ai movimenti dei tassi, portando a oscillazioni di prezzo più pronunciate durante tali movimenti.

Al contrario, le obbligazioni a bassa convexity subiscono meno variazioni di prezzo in caso di cambiamenti dei tassi, generando una tipica curva a U quando tracciate in un grafico bidimensionale, da cui il termine "convex". Le obbligazioni a basso cedola e le zero-coupon, con rendimenti più bassi, manifestano una maggiore volatilità rispetto ai tassi. Ciò implica che la modified duration dell'obbligazione richiede un aggiustamento più ampio per allinearsi con l'amplificazione delle variazioni di prezzo dopo scosse dei tassi. Il rapporto inverso tra tassi cedolari, rendimenti e convexity persiste, accentuando l'interazione dinamica nella sensibilità ai tassi di interesse.

Conclusione

Investire a reddito fisso può essere impegnativo a causa della natura sempre mutevole dei tassi di interesse, che crea incertezza. Per affrontare questa sfida, gli investitori usano duration e convexity come strumenti per quantificare l'incertezza e gestire efficacemente i portafogli a reddito fisso.